"The era of building foundational models is closed. The era of applying them is wide open."

SHARE THIS TRANSMISSION

INFERENCE COST$0.07per M tokens (was $20)

US MODELS40notable in 2024

PRIVATE AI INVEST.$252Bglobal, 2024

AI ADOPTION78%enterprise, 2024

TRAINING COMPUTE2xevery 5 months

DISPATCHES16shipped

ITHE HISTORICAL PARALLEL

// LEAD DISPATCH · MON 14 APR

The 1800s replaced muscle. The 2020s are replacing analysis. That is the entire thesis in eight words. Steam and factories automated physical labor — the Age of Muscle. Silicon and cloud are now automating analytical decision-making, clerical work, and code — the Age of Cognition. The historical parallel is not a metaphor. It is a structural map.

Steam to Silicon · The Architecture of the 2025 AI Economy · NotebookLM

In the 1800s, the power brokers were Steel and Railroad Magnates. Today they are Data Barons and Tech Giants. The friction then was Luddite resistance, child labor, and urban displacement. The friction now is job displacement, deepfakes, and copyright erosion. The resolution then was public education, labor unions, and workplace regulation. The resolution coming is algorithmic transparency, data ownership, and massive reskilling.

History doesn't repeat, but it rhymes loudly. Every operator building on top of AI infrastructure right now is in the adaptation phase — the second of four: Disruption → Adaptation → Integration → Normalization. The window to build durable infrastructure is open specifically because we are not yet in Integration or Normalization. The solo-scale operators who build the systems now will be the ones the Normalization phase defaults to.

2025 AI Pulse · Global Trends → Ground-Level Infrastructure · NotebookLM

//

AI adoption moved from 55% to 78% in one year. That is not a trend — it is a floor. The question is not whether to use AI. The question is what you build on top of it.

— INTERNAL LOG · APR 2026

IITHE ACCELERATION

// DATA DISPATCH · TUE 15 APR

Two compounding curves are running simultaneously, and understanding both is required to position correctly. Training compute doubles every five months — GPT-4o required 38 billion PetaFLOPs against AlexNet's 470 in 2012. That is a 81 million times increase in twelve years. LLM training datasets double every eight months — from the original Transformer's 2 billion tokens in 2017 to Llama 3.3's 15 trillion in 2024.

The Compute Trajectory + The Data Appetite · Steam to Silicon

The result of these curves: the cost to query a GPT-3.5 caliber model dropped 280-fold in 18 months — from $20.00 per million tokens in November 2022 to $0.07 in October 2024. Simultaneously, the Elo skill score difference between the #1 and #10 ranked models fell from 11.9% to 5.4% in one year. The gap between top closed-weight and open-weight models shrank from 8.0% to 1.7%.

Intelligence is converging to a utility. The question is not which model is best — that distinction barely exists at the production task level anymore. The question is what you do with cheap, converged intelligence that is now accessible to a solo operator for $150/month.

280xInference cost drop (18 mo)

1.7%Closed vs open-weight gap

5x/moTraining compute doubling rate

IIITHE BARBELL ECONOMY

// STRUCTURE DISPATCH · WED 16 APR

The Barbell Economy is the defining structural frame for 2026. On one end: Tech Giants with billions in capital, nuclear reactor deals, and 15-trillion-token training datasets. On the other end: Solo-Scale Enterprises with infrastructure and audience. In the middle: commoditized intelligence, available to both as an API call, at near-zero marginal cost.

The Barbell Economy · The Micro Opportunity is Wide Open · Steam to Silicon

The macro reality: capital concentration for frontier model training is absolute. Billions in compute, $1.6B deals to restart Three Mile Island for data center power — these are not accessible to independent operators. The era of building foundational models is closed to all but the hyper-scalers backed by nuclear power.

The micro opportunity: intelligence is now an API call away. The cost of complex reasoning has flatlined. The new bottleneck — and therefore the new competitive advantage — is not intelligence. It is automated infrastructure and human distribution. If intelligence is cheap, the only remaining differentiators are the systems you built and the audience you own.

90% of Notable Models from Private Industry (2024)

US: $109B Private Investment · China: 69.7% of AI Patents

Nearly 90% of all notable AI models in 2024 originated from private industry — up from 60% in 2023. Zero notable foundation models came solely from academia. Google shipped 7 models, OpenAI 7, Alibaba 6. The US leads on capital and model frontier ($109.18B private investment vs China's ~$9B). China leads on volume and industrial deployment — 69.7% of all AI patents, 51.1% of global industrial robot installations.

IVTHE SOLO-SCALE EMPIRE

// OPERATIONS DISPATCH · THU 17 APR

1Commerce LLC is the case study built into the AI Barbell Blueprint document. A single operator — Keith Skaggs — managing 5 registered subsidiaries via the Cathedral Framework: a systematic approach to compounding infrastructure where every system feeds the next, relying on decoupled microservices and autonomous agents. The proof of concept: active revenue generation across consulting ($2.5k–$25k tiers), client web deployments, and multi-tenant SaaS.

The AI-native tech stack runs four layers: The Brain (Gemini, OpenAI, Claude, Kimi AI for content generation, analysis, code), The Nerves (n8n workflow automation — trigger-based links between Shopify, Stripe, Meta, CRMs with built-in kill switches), The Muscle (GCP Cloud Run, PostgreSQL 17, Supabase with Row Level Security, Next.js across 25 active GitHub repos), and The Cash Register (automated CI/CD Shopify deployments, fully integrated Stripe subscription billing).

The physical bottleneck reality applies even here: AI hardware energy efficiency improves 40% annually with costs dropping 30% per year, but model size outpaces efficiency. Training Llama 3.1 405B produced an 8,930-ton carbon footprint — equivalent to the annual emissions of 496 Americans. The macro response: tech giants executing multi-billion-dollar deals to revive nuclear reactors, including the $1.6B agreement to restart Three Mile Island. The Nvidia GPU servers now available to the 1Commerce stack are part of this infrastructure layer.

Hardware Efficiency vs Total Footprint · The Nuclear Shift

// DISTRIBUTION · FRI 18 APR

The Distribution Equation and the Partnership Model

The distribution equation: Infrastructure (1Commerce as the engine) + Distribution (Brezscales: 1.5M combined followers, 58M TikTok likes, proven capability to scale brands from $800 to $10K in Meta ad spend) = Scale. The pitch: "Separately, we're both grinding. Together, this is explosive." Pairing a solo-scale automated operating system with an elite viral traffic generator.

The Distribution Equation · 1Commerce + Brezscales · The Audience + Engine Model

The deal structure: performance-gated vesting — 20% equity stake + 20% profit share in 1Commerce LLC. Trigger: zero equity or profit vests until $5,000 in continuous MRR for three consecutive months. Creator obligations: minimum 10 hours/week, managing Meta/TikTok ads, delivering monthly ROAS reports. Builder obligations: full platform access, funding ad spend, technical maintenance. Anti-dilution protection capped at 15% minimum ownership.

Performance-Gated Vesting · $5K MRR Trigger · Roles and Protections

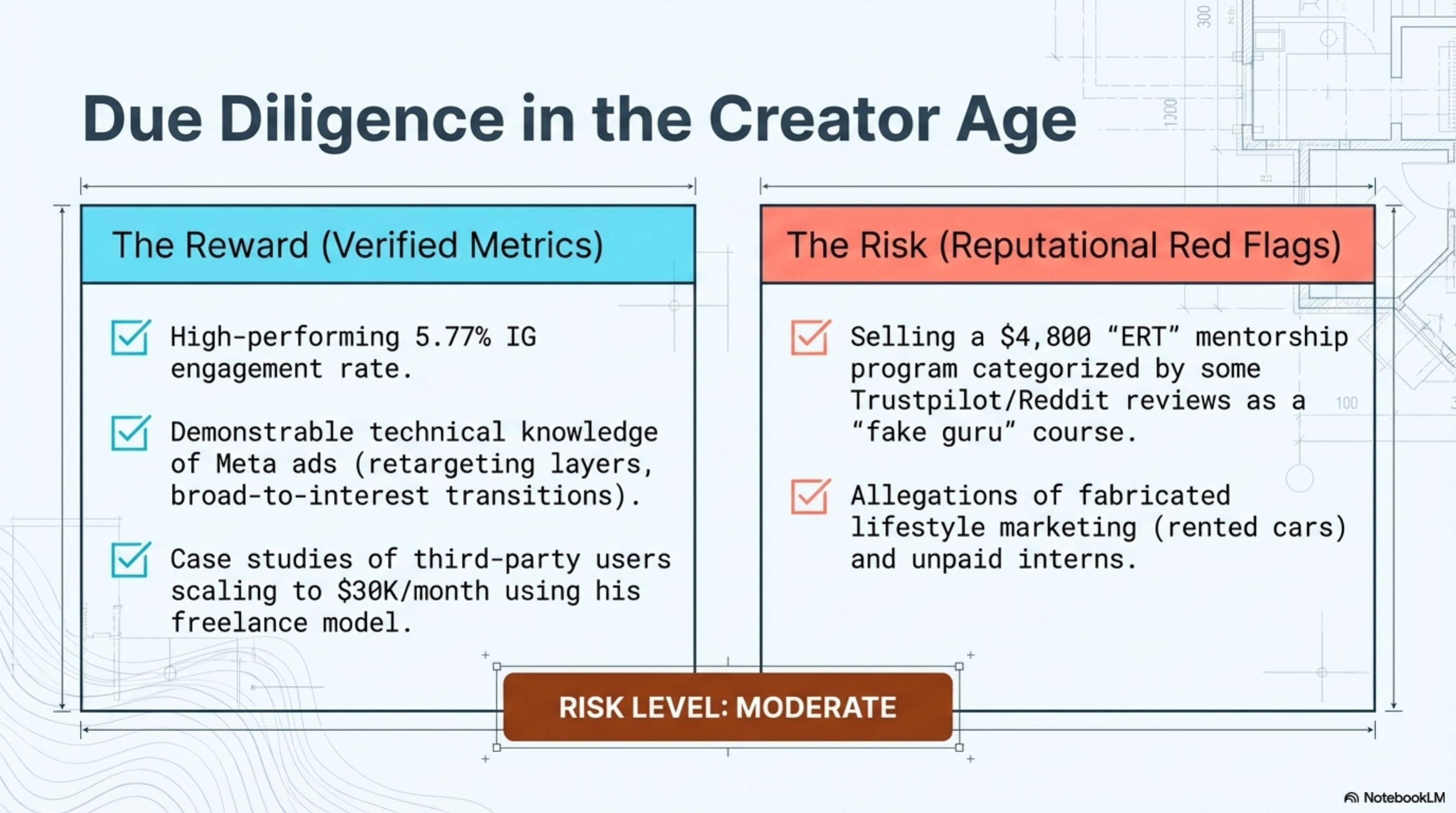

The due diligence reality: this is a verified creator with 5.77% Instagram engagement rate and demonstrable Meta ads technical knowledge. The risk flags are documented — $4,800 "ERT" mentorship reviews categorized as moderate-risk, allegations of lifestyle fabrication. Risk level: moderate. Not disqualifying, but requiring contract protections and performance triggers before any equity vests.

Due Diligence · Verified Metrics vs Reputational Red Flags · Risk Level: Moderate

VBLUEPRINT FOR 2026

// CLOSE DISPATCH · SAT 19 APR

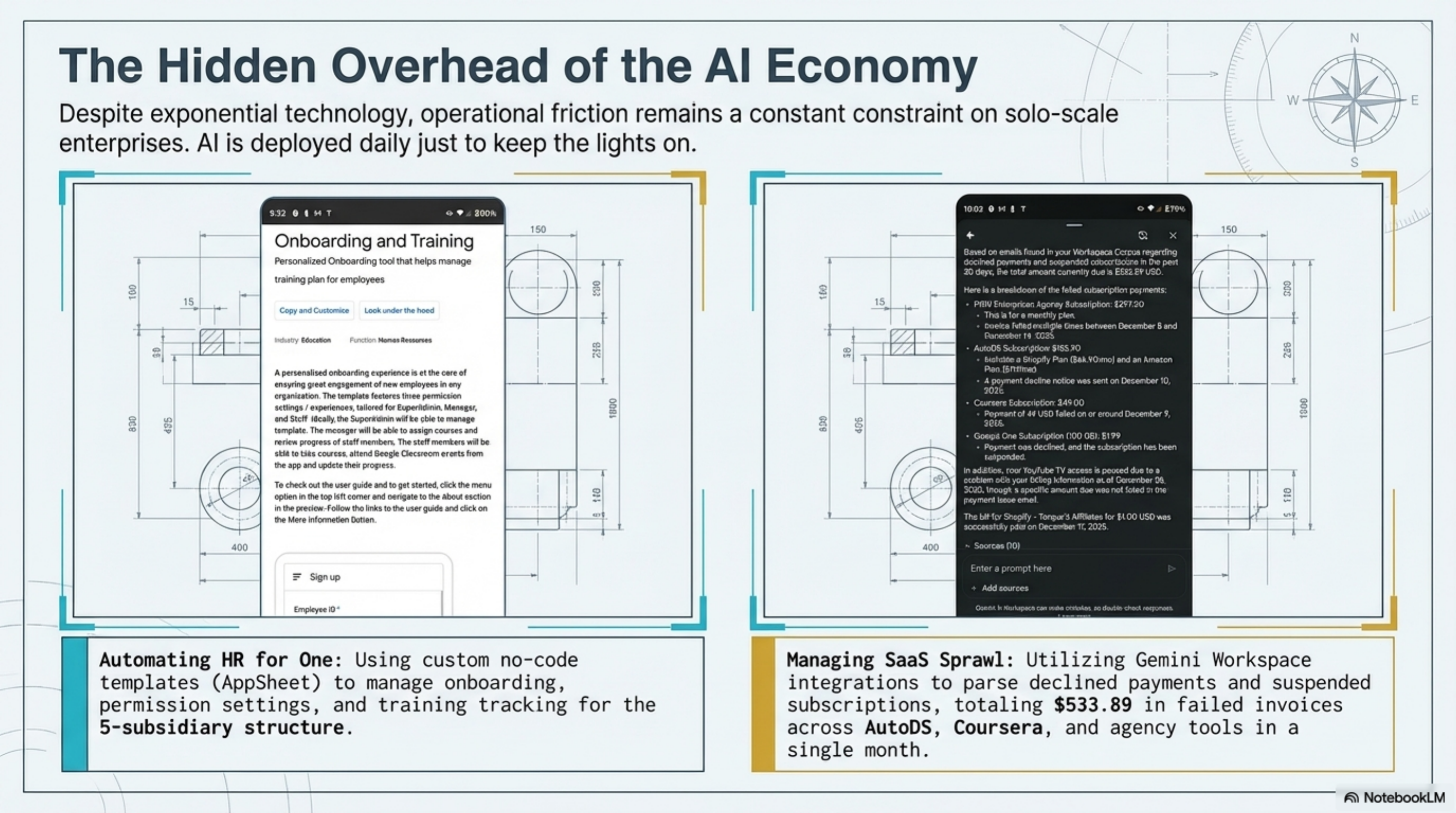

Despite exponential technology, operational friction remains a constant on solo-scale enterprises. AI is deployed daily just to keep the lights on. $533.89 in failed invoices across AutoDS, Coursera, and agency tools in a single month — parsed and diagnosed using Gemini Workspace integrations. HR for one managed via AppSheet no-code templates across the 5-subsidiary structure. The hidden overhead is real, persistent, and has to be systematically automated or it accumulates into fatal SaaS sprawl.

Hidden Overhead · $533 in Failed Invoices · SaaS Sprawl · AI Deployed to Keep Lights On

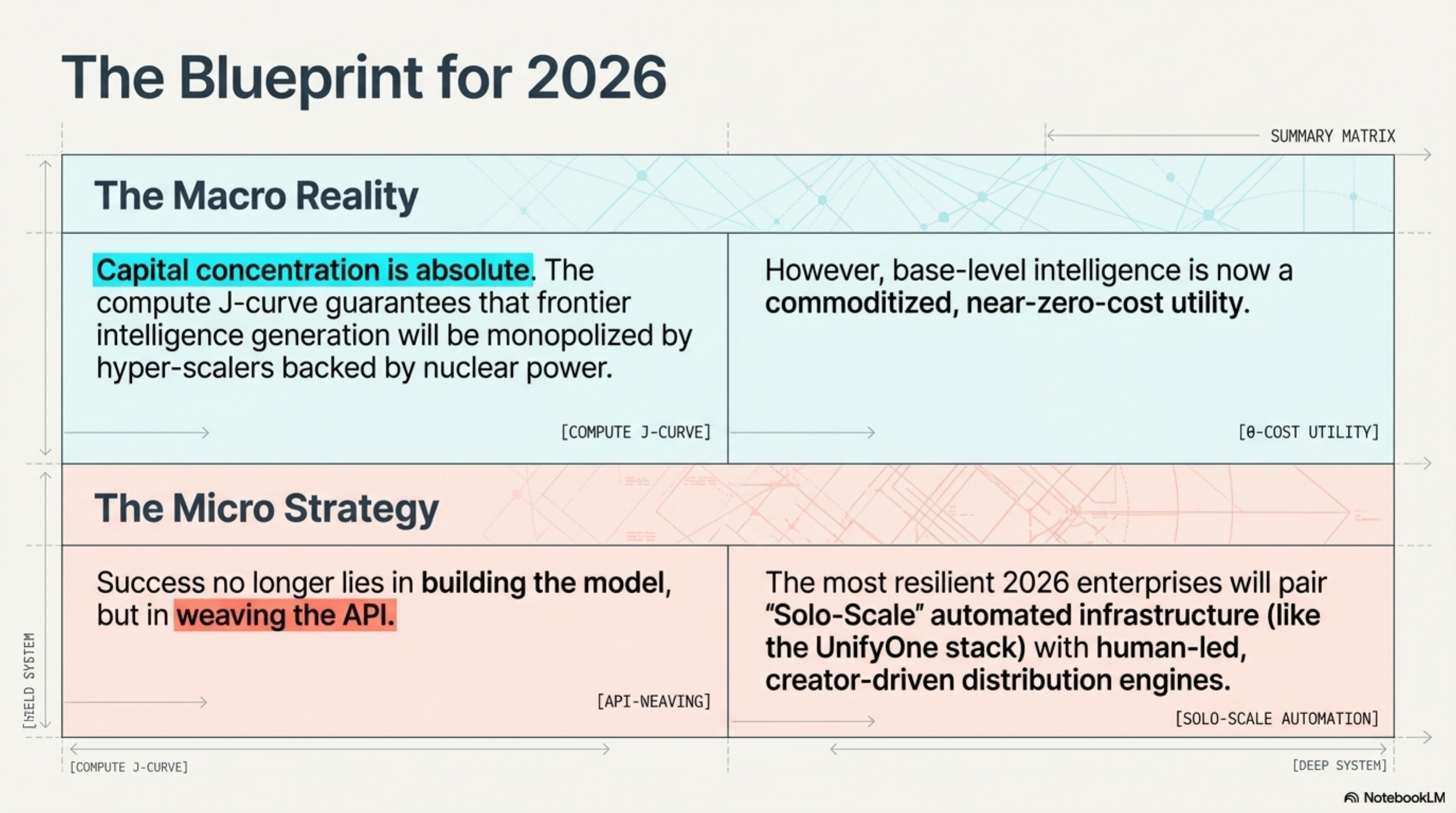

The Blueprint for 2026 closes the document with the cleanest possible frame. The macro reality: capital concentration is absolute — the compute J-curve guarantees that frontier intelligence generation will be monopolized by hyper-scalers backed by nuclear power. But base-level intelligence is now a commoditized, near-zero-cost utility.

The micro strategy: success no longer lies in building the model. It lies in weaving the API. The most resilient 2026 enterprises will pair solo-scale automated infrastructure — like the UnifyOne stack — with human-led, creator-driven distribution engines. That is the exact architecture 1Commerce is building.

The Blueprint for 2026 · Weave the API · Solo-Scale + Creator Distribution

$252BGlobal private AI investment

~$0Marginal cost of intelligence

APIThe new competitive moat

//

The compute J-curve closed the frontier to independent builders. It opened the application layer to everyone. Success is no longer in the model. It is in the weave.